Evaluating Publicly Traded Companies Using Venture Capital Methods

How many of the top five S&P 500 companies by market cap would you imagine are technology companies? All 5.

When it comes to valuing fast growing tech companies, venture capitalists seem to speak in their own foreign language. Traditional Wall Street terms like earnings per share, return on assets or discounted cash flows don’t even exist in their dictionary. That’s because VCs care about one thing and one thing only – top line growth, and because they’ve spent decades fixating on this single line-item, they’ve gotten really good at quantifying its value.How many of the top five S&P 500 companies by market cap would you imagine are technology companies? All five.It seems that Marc Andreessen of Andreessen Horowitz was right when he wrote his op-ed in 2011, high growth technology companies are eating the world. With so many tech companies set to enter the public markets over the next decade, you simply cannot write them off any longer. It is of existential necessity that investors understand the right ways to evaluate these types of companies. We cannot limit our world to conventional wisdom around dividend payouts and PE ratios – we need to know what the VCs know.

Learning basic vocabulary in the VC language. Quantifying efficient growth.

There are a number of VC metrics that we can carry over into the public arena. One in particular is the Bessemer Efficiency Score, made popular by Bessemer Venture Partners. This formula is used to quantitatively indicate how efficiently a company is growing, which helps answer the question we all have when we watch Amazon break past $1 trillion in market cap – is the growth worth it?The Bessemer Efficiency Score formula is as follows, where ARR is Annual Recurring Revenue and FCF is Free Cash Flow.

Bessemer Efficiency Score (BES) = ARR growth + FCF margin

Because publicly-traded companies do not openly disclosed ARR numbers, we’ve modified the formula. Using gross margin growth instead of simply revenue growth, we capture more visibility into the quality of revenue:

Mirador Modified BES (MMBES) = Gross margin growth + FCF margin

In certain cases we may even adjust the formula to account for certain factors. For example, to account for leverage we may include a debt factor:

Adj MMBES= (Gross margin growth+FCF margin) (1 -%debt/2)

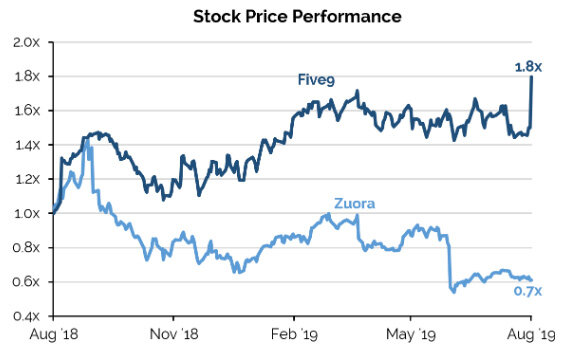

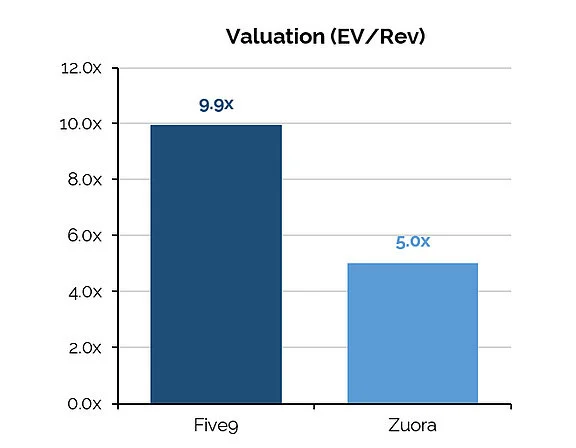

Let’s see how the MMBES works in practice with a Mirador Tri-Valley Index portfolio company, Five9.

Both are high growth software companies, both generate a similar level of revenue, both have similar gross margin profiles and both generate negative GAAP profits. You can’t judge these companies off of earnings so you’d have to look at revenue growth. Unfortunately you’d be completely wrong if you just did that. Even though Zuora has a higher growth rate than Five9, Zuora’s stock has significantly underperformed and trades at a half the valuation to Five9. The key is to look at how efficient that growth is, and according to the MMBES Five9’s growth is 2x more efficient. In other words, Zuora burns twice the amount of cash that Five9 does to get the same level of growth.

Speaking VC in the public markets

MMBES works extremely well in explaining the valuations behind technology stocks. Below we’ve charted all of the Technology Service companies in the S&P 500 Index.

As you can see, the magic behind valuations goes from a soft art to a dead-on science when applying MMBES.

We can also apply the principle of MMBES to other industries. Although each industry requires adjustments, the core formula does a phenomenal job quantifying the balance between growth and spend, as well as valuation.

I feel it is necessary to say that MMBES is not an end-all-be-all tool and should be used in conjunction with other financial tools out there, but it is a good indicator that quantifies how much a company needs to spend in order to grow. There is much that stock market investors can learn from VCs. We don’t need to speak their language, but we at least need to understand.

After all, they are ones building this next generation of publicly traded companies – they might have a good perspective on how to evaluate them.

I want to receive Mirador’s research and market updates!

Information presented reflects the personal opinions, viewpoints and analyses of the employees of Mirador Capital Partners, LP, an SEC-registered Investment Adviser. The views reflected in the commentary are subject to change at any time without notice. Nothing herein constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Mirador Capital Partners, LP manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results. Visit us at miradorcp.com for more information.