Bubble Shooter

In today’s market environment, managing risk in a portfolio can be difficult. Some investors will beat themselves up for missing out on what may turn out to be one of the largest bubbles of our lifetimes, while others will never forgive themselves for not getting out in time. The majority of people will, unfortunately, end up doing both, as they did in $GME. This uncontrollable urge is called FOMO, but let’s give the risk behind it a name – Bubble Risk.

It is important for the investor to be able to identify the specific kind of risk in their portfolio. While raising cash and allocating to bonds is the traditional blanket method for risk reduction, it is overly simplistic and does not effectively address the current risks we face, namely Bubble Risk. Also, the combination of negative real interest rates, an inflation-obsessed Fed, and deficit-agnostic fiscal policy has created a TINA market (There Is No Alternative), where holding cash and bonds is a form of capital destruction and stocks are the only source of returns.

Let’s conceptualize Bubble Risk using an analogy we are all familiar with: home buying. Below are two homes I found on Zillow that are currently selling in/around Palo Alto.

Based off the price/sqft., it is clear that a buyer is getting massively more value with the Humble Abode than they are the Chateau. Granted, the Chateau buyer always finds ways to argue otherwise, “The door handles are solid ivory.” or “The infinity pool is to die for.” They may be right, but for simplicity purposes we’ll focus on the most primal reason to even buy a house – for space to live in. At $2,889/sqft. the price of the Chateau has deviated far from the fundamental value it provides. Buyers instead justify the valuation based on extrinsic factors like the better school district, the imported ceiling moldings or who the neighbors are – all important aspects to home ownership, but subjective in value. Thus the value of the home is largely determined by the subjectivity of the buyer.

This is important to understand because if the only reason I bought the Chateau for $23M was because I liked it, then who knows how far the price can drop if the next buyer doesn’t. We can see this pricing volatility in the Zillow price estimate history. The estimated value of the Chateau dropped 50% ($10M downswing) in 2019, then proceeded to triple over the following year ($20M upswing, whoever said real estate is a stable investment?) These swings aren’t just theoretical, we see if all the time in the ultra-wealthy housing market. In 2017, Ellen DeGeneres purchased a Montecito estate next to Oprah’s for $7M and flipped it 12 months later for $11M or a 57% profit (everyone likes Oprah right?) Unfortunately for Eva Longoria, Kanye West must have moved in next door because she purchased her Hollywood home from Tom Cruise in 2015 for $14M, but only got $8M for it last year, netting $6M or 42% loss.

Price fluctuations of the Abode, on the other hand, are nonexistent. While the Chateau was making volatile swings, the Abode remained pegged near $1M. Why? Because despite being situated in East Palo Alto, a tiny lot and a 2/10 elementary school rating, $636/sqft. is dirt cheap in any environment anywhere within a 50mi radius.

Bubble Risk introduces violent price swings

In no environment, would an investor ever want to bet that the price of the Chateau will decline over time. After all, ivory is precious and everyone loves Oprah. And if someone with the means is willing to spend on it today, it’s difficult to argue why they wouldn’t tomorrow. Most importantly though, if the price triples overnight, the cost of being wrong could be career-ending. Think Tesla short sellers and Melvin Capital. If you must bet on a direction, and there is no reason to explain why the price is as high as it is, then all you can do is hope that it goes higher.

Today’s stock market, like the Chateau, faces that same Bubble Risk. Negative real interest rates and continued fiscal stimulus (can we still call if stimulus if it never stops?) has created an inflationary environment that has propelled stock valuations (price/sqft.) into the stratosphere. It is becoming impossible to intellectually explain why an investor would continue to purchase stocks at their current valuations. The only explanation is a subjective one, currently gaining popular among internet day traders – “We like the stock.”, just like the Chateau buyers like Oprah. When the sentiment swings though, so will the price.

Managing Swings with Insurance

When prices have the potential to swing, one of the ways to preserve capital is through the purchase of insurance. Unfortunately there is a strange paradox to how insurance works. In theory, you pay a small fee today, before a possible catastrophe occurs, to protect against the downside. In reality the opposite occurs. For example, demand for earthquake insurance is always the highest and the most expensive after a major earthquake has already hit. This makes insurance both costly and ineffective for the average person, but for a savvy investor it presents a strange opportunity – insurance is always in the lowest demand, and the cheapest, prior to a catastrophe.

The chart below shows the relationship between the VIX (Volatility Index) which can be interpreted as the cost of insurance against major stocks market swings, and investor sentiment represented by the S&P500 corporate risk premium. In line with our earlier opportunity, the VIX is always the cheapest prior to equity selloffs when investors are the most bullish. In a perfectly logical world, this wouldn’t be the case and the blue and gold lines would instead be mirror images of each other. Thus understanding this disconnect between what should be and what is can help investors create more resilient portfolios when Bubble Risk is present.

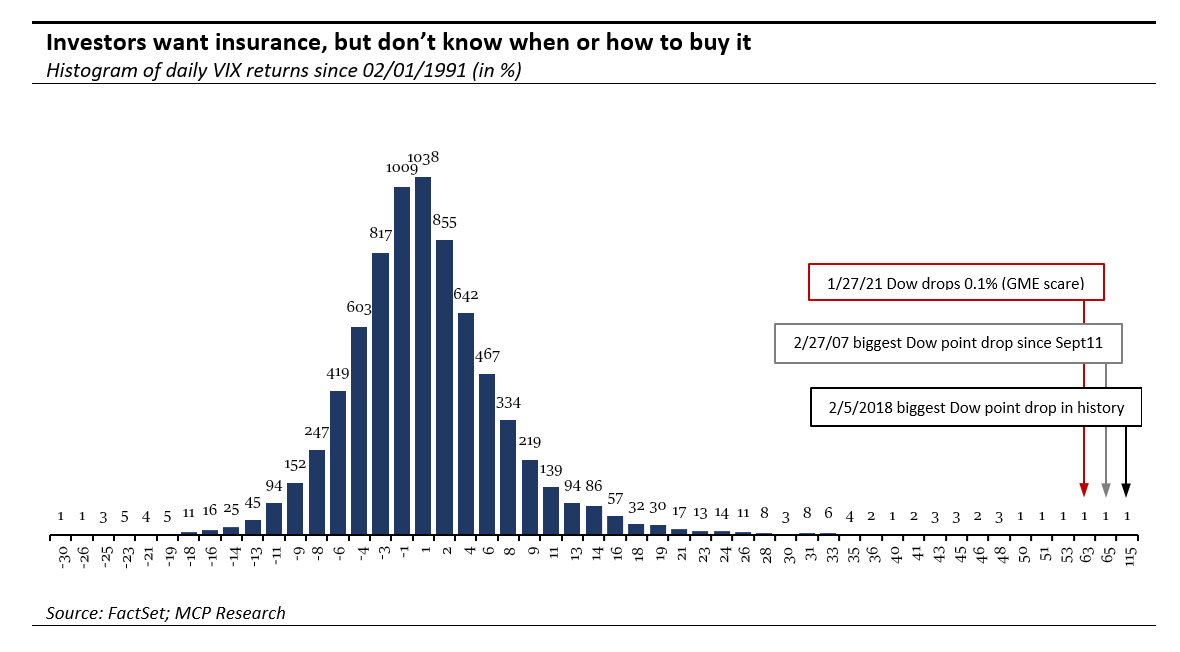

An interesting point to note is the strong bid for insurance ever since the COVID-19 selloff. Since Feb 2020, the VIX has remained above 20. That is considered high by historical standards, and would imply limited upside potential, but that thinking hasn’t materialized in practice. In fact, of the six biggest daily VIX moves since 1991, two of them were in the last eight months. Major spikes in the VIX use to occur alongside severe market drawdowns, but recent spikes have been against a rather muted backdrop. This should give investors who are looking to incorporate insurance into their investing even more confidence – the market seems aware of the importance of insurance, but still unable to grasp the timing and implementation.

I want to receive Mirador’s research and market updates!

Information presented reflects the personal opinions, viewpoints and analyses of the employees of Mirador Capital Partners, LP, an SEC-registered Investment Adviser. The views reflected in the commentary are subject to change at any time without notice. Nothing herein constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Mirador Capital Partners, LP manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results. Visit us at miradorcp.com for more information.